What Is Blockchain? How are Blockchain & Cryptocurrencies Linked? What Are The Different Types & Uses Of Blockchains and Cryptocurrencies?

What Is Blockchain? How are Blockchain & Cryptocurrencies Linked? What Are The Different Types & Uses Of Blockchains and Cryptocurrencies?

Not all cryptocurrencies—and not all blockchains that the various cryptocurrencies rely on—are created equal. All cryptocurrencies rely on one form of blockchain technology or another to function—without blockchain technologies, cryptocurrencies would have no reliable way of handling the kind of decentralized, “trustless” accounting necessary to ensure a hack- and tamper-proof ledger of transactions.

It can be quite challenging to attempt to summarize all of the various blockchain technologies currently in existence—there are currently thousands of them. An easier way to go about doing this is first to look at the kind of blockchains currently in existence in a general sense, and then move on to a discussion of the various types of cryptocurrencies themselves.

Different Types Of Blockchains

Before discussing the different types of blockchains, it would be useful first to have an understanding of blockchain technology in general. Blockchain technology, defined at perhaps its most simple, is a distributed accounting ledger that is used to record transactions in a tamper-resistant, verifiable, and permanent manner. When blockchain technology is described as “open,” it refers to the open-source code that most blockchain protocols are built on.

Blockchain technologies can be either public (like Bitcoin) or private and still use this open-source code. Sometimes, you’ll see the term “distributed ledger” used to describe certain types of blockchains. This is really just another way of saying “decentralized,” as the continually developing ledger which records transactions are shared by multiple participants in the blockchain and is not owned or controlled by a single central authority.

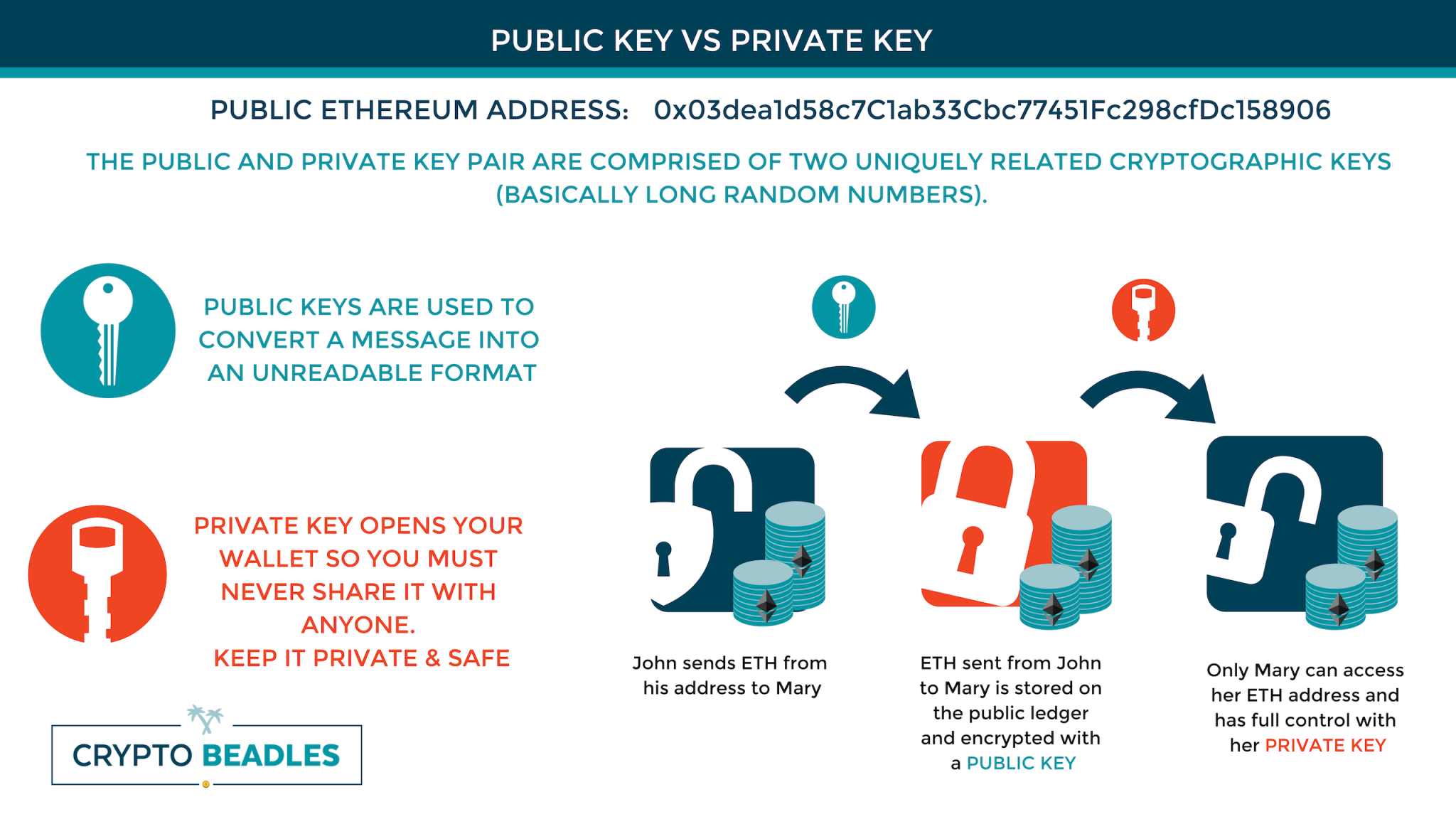

Blockchain technology allows efficient accounting of any transaction between two parties, largely because there is no need to rely on a third party (like a bank, in traditional financial transactions) to verify or facilitate the transaction. A transaction is mutually agreed upon by the parties involved—an exchange of a set amount of cryptocurrency between crypto wallets, for instance—and is then entered into the ongoing ledger—the next block on the chain.

Once entered and verified by the blockchain network, the transaction is permanent and can’t be altered in any way. The various cryptographic schemes (like proof of work or proof of stake) behind these blockchains allow for both the accurate recording and verification of the transactions, resulting in a hack-proof system.

It can perhaps get a bit confusing with the new applications that blockchain technology is being used for. There are, in effect, three primary kinds of blockchains, if you’re not counting databases or distributed ledger technology, which are both built on the same technological foundations.

Public Blockchains

There are public blockchains—such as the kind used by Bitcoin, Ethereum, and in fact every other form of cryptocurrency. This type of blockchain is generally open-source and “democratic,” allowing anyone to participate simply as users making transactions through the blockchain, or as “miners.” Miners (called Validators in Ethereum) verify the validity of new blocks by solving complex mathematical “puzzles” through a proof of work protocol and are awarded a unit of cryptocurrency for their efforts.

Members of the public are also allowed to participate as community members and even to an extent as developers, suggesting or in some cases implementing advances and refinements in the way the blockchain functions. A good example of this is the Ethereum blockchain: though still using proof of work protocols for validation of new blocks, there has been substantial discussion of moving to a proof of stake system, which brings with it significant energy savings as it relies on one node for the validation of new blocks instead of many nodes all engaged in redundant work, in a race to “solve” the next new block.

Most significantly, all transactions recorded on a typical public blockchain are fully transparent and allow anyone to examine the details of any (and all) transactions. Refinements in blockchain technology allow for public blockchains with “private” functionality, which is blockchains that operate in much the same way as the Bitcoin public blockchain, but which are still capable of securely processing transactions, as we’ll see below in the discussion of so-called “private coins.”

Public blockchains are built to be completely decentralized, meaning there is no central authority, individual, or other entity controlling which transactions are entered into the ongoing ledger that makes up the blockchain or dictating the order in which they are validated and processed. Public blockchains are meant to be resilient, tamper-proof, and “censorship-resistant.”

This is accomplished by allowing anyone to join the network and run a full blockchain node, regardless of their geographical location, nationality, or other signifying characteristic. Because of this, it is next to impossible for governments or other would-be regulating authorities to interfere in the operation of a public blockchain.

Private (and Consortium) Blockchains

There are private blockchains—examples would be things like R3 Corda and Hyperledger. Also, sometimes called “permissioned” blockchains, private blockchains are different in a number of significant ways from public blockchains. In order to join the network of devices that runs a private blockchain, a would-be participant must first be granted consent.

Transactions are, therefore, more private, and are only available to those who have already been given permission to join the network. Private blockchains, while often not fully centralized, are much more centralized in nature than public blockchains, as they rely on something like a central authority to grant permission and oversee transactions. The authoritative bodies running a private blockchain have significant control over both participants and development (or “governance”) structures.

Private blockchains are most commonly used by enterprises who want to share data and collaborate by utilizing or accessing it, but naturally don’t want their proprietary business information available to any member of the public, which would be the case with a public blockchain.

Consortium Blockchains

Also sometimes called “confederated” blockchains, these are an offshoot of private blockchain technology, and are essentially the same as private blockchains with the marked difference that they rely on a group of authorities rather than a single entity. This allows different entities—in theory, different corporations, for instance—to collaborate using data available to every member of the consortium. Though they may be in direct or indirect competition, by sharing data that is common to their interests, they are able to collaborate effectively, and there is mutual benefit from such an arrangement. Consortium blockchains, it is hypothesized, will likely see use by entities like governments, banks, financial institutions, and corporations in the procurement, logistics, and supply chain sectors.

Types of Cryptocurrencies

Also sometimes called “confederated” blockchains, these are an offshoot of private blockchain technology, and are essentially the same as private blockchains with the marked difference that they rely on a group of authorities rather than a single entity. This allows different entities—in theory, different corporations, for instance—to collaborate using data available to every member of the consortium. Though they may be in direct or indirect competition, by sharing data that is common to their interests, they are able to collaborate effectively, and there is mutual benefit from such an arrangement. Consortium blockchains, it is hypothesized, will likely see use by entities like governments, banks, financial institutions, and corporations in the procurement, logistics, and supply chain sectors.

Payment Currencies

Cryptocurrencies of this type are intended for the payment of goods and services. Payment currencies can be used for transactions between private parties for whatever purpose, or (as is increasingly the case with Bitcoin) can be used to pay for tangible items in “the real world.” More businesses are accepting Bitcoin as a payment every day, and in some cases, local governments have moved toward accepting the cryptocurrency as a form of payment for things like parking tickets. In almost every case, payment currency cryptocurrency can also be “cashed out” from their digital form in exchange for local fiat currencies like the dollar, the euro, etc. Examples of well-known payment currencies are Bitcoin (BTC), Bitcoin Cash (BCH), Ethereum (ETH), Tether (TUSD) and Litecoin (LTC), among others.

Blockchain Economies

This is often argued as a step forward in the concept of digital, decentralized currency. A blockchain economy, which is often also called simply a blockchain platform, utilizes blockchain technology in broader, more innovative ways. Instead of merely existing to keep a record of various cryptocurrency transactions, blockchain economies allow their users to create things like discrete digital assets (most commonly referred to as tokens) and decentralized applications (DAPPS) that use the underlying blockchain technology as a basis for transactions of a different type.

In one notable instance, a cryptocurrency called Golem (GNT), while distinct and separate from the cryptocurrency primarily supported by the Ethereum blockchain (commonly also called Ethereum, but more correctly called Ether), exists entirely on the Ethereum blockchain. The value of Golem is not tied to that of Ether—it merely “piggybacks” on the Ethereum technology, which is designed in such a way as to make the creation of “tokens” like the Golem cryptocurrency possible.

Though this is an example of a cryptocurrency within a blockchain economy, the economies themselves are also used for the support and payment of things like virtual assets, processing power, the running of dependent applications, and many more various (and imaginative) purposes.

Perhaps the most notable cryptocurrencies falling under the example of blockchain economies would be Ether (ETH), Ethereum Classic (ETC), BCH (SLP), EOS (EOS), NEO (NEO), and Tron (TRX).

Privacy Coins

This is often argued as a step forward in the concept of digital, decentralized currency. A blockchain economy, which is often also called simply a blockchain platform, utilizes blockchain technology in broader, more innovative ways. Instead of merely existing to keep a record of various cryptocurrency transactions, blockchain economies allow their users to create things like discrete digital assets (most commonly referred to as tokens) and decentralized applications (DAPPS) that use the underlying blockchain technology as a basis for transactions of a different type.

In one notable instance, a cryptocurrency called Golem (GNT), while distinct and separate from the cryptocurrency primarily supported by the Ethereum blockchain (commonly also called Ethereum, but more correctly called Ether), exists entirely on the Ethereum blockchain. The value of Golem is not tied to that of Ether—it merely “piggybacks” on the Ethereum technology, which is designed in such a way as to make the creation of “tokens” like the Golem cryptocurrency possible.

Though this is an example of a cryptocurrency within a blockchain economy, the economies themselves are also used for the support and payment of things like virtual assets, processing power, the running of dependent applications, and many more various (and imaginative) purposes.

Perhaps the most notable cryptocurrencies falling under the example of blockchain economies would be Ether (ETH), Ethereum Classic (ETC), BCH (SLP), EOS (EOS), NEO (NEO), and Tron (TRX).

Utility Tokens

On a blockchain that supports it, the creation of a “token” is similar to, but not the same as, the creation of a unit of cryptocurrency. For a token to qualify as a utility token, there is, however, a strict set of legal regulations and requirements. We won’t go into those requirements here, but one example of a token that is currently considered a utility tokens is Binance’s “BNB” token. This token was initially created to allow for owners of the token to pay for trading fees with a discounted rate on the Binance Exchange.

Utility tokens can sometimes be digital tokens used in transactions to pay for or fund blockchain-based services or products. They typically run on a blockchain platform—which you’ll remember is another name for a blockchain economy. The most popular utility tokens to date are based on the Ethereum blockchain, but as new blockchains come into existence all the time, other blockchains have (and will continue to) spawn their own tokens.

Aside from BNB, other notable examples of utility tokens include the Basic Attention Token (BAT), Civic (CVC), OmiseGo (OMG), Monarch Token (MT), and 0x (ZRX).

Stablecoins

Lastly, there are stablecoins, so-called because (unlike other cryptocurrencies), they are intended to hold a fixed value and be traded at the same price, without market fluctuations being a factor. This kind of cryptocurrency is popular among investors and other traders of different kinds of cryptocurrency, as they represent a way to possibly hedge against possible losses in the secondary cryptocurrency being used to pay for the stablecoin.

For instance, say an investor holds $1,000 worth of Bitcoin. If that investor suspects that the value of the Bitcoin is likely to decrease in the near future, he or she could buy $1,000 worth of a stable coin asset, thereby divesting the held Bitcoin and being protected from the (assumed) devaluation. This, in theory, should protect the trader from financial loss—if his or her instincts are correct. However, with all things that have to do with money, there’s no such thing as a guaranteed thing. Everything has risks, and one must do their due diligence and contact professional financial advisors before making any decisions. Please note, this article is not financial advice, but to help give you a better understanding of the blockchain and cryptocurrency landscape.

The methods that different stablecoins use to maintain a fixed price vary. Stablecoins can be tied to a currency—for instance, a hypothetical stablecoin could be said to always be worth $1 USD. Though the value of that $1 USD may fluctuate, the stablecoin will always be exchangeable (at least in theory) for $1 USD. Like other commodities traded on traditional stock markets, stablecoins can also be tied to real-world commodities like precious metals, or in some cases, “baskets” of commodities, as is commonly done in traditional market investing.

Notable examples of stablecoins would include Dai (DAI), Gemini (GUSD), Paxos (PAX), Tether (USDT), TrueUSD (TUSD), and USD Coin (USDC).

Conclusion:

** This is not financial advice and these are simply my own opinions, as such, this should not be treated as explicit financial, trading or otherwise investment advice. This is not explicit advice to buy these cryptos, do you own research.**

***Disclaimer: Statements on this site do not represent the views or policies of anyone other than myself. The information on this site is provided for discussion purposes only, and are not investing recommendations. Under no circumstances does this information represent a recommendation to buy or sell securities.

***ALWAYS check with professional tax service providers and legal professionals before you buy, sell or trade cryptos!

Thanks for reading, God Bless and have an awesome one!

Be sure to check out our other articles on to cryptocurrency, bitcoin and blockchain technology below:

“Blockchain: What It Is and How It Works”; which delves into the history of blockchain, how blockchain works, how cryptocurrency uses blockchain, discusses anonymity, various types of blockchains and the different uses.

“What is Ethereum? How does Ethereum work? ETH Explored:” Dive deep into one of the largest blockchains, discover how it is different from Bitcoin and other cryptocurrency projects.

“How To Store Cryptocurrency / Safeguard Your Crypto Assets”; which discusses the most popular cryptocurrencies, how to protect your crypto, online wallets, offline storage, specialty hardware, crypto exchanges, and even gives Crypto Beadles Personally Recommendation with storing cryptocurrencies.

“Scrubbing Currency: A Comparison of Crypto to Fiat for Known Money Launderings”; This article dives into the various efforts to curb money laundering, typical money laundering with fiat currency problems faced by authorities worldwide, the rise of cryptocurrency, the differences between traditional fiat and cryptocurrencies, the history of traditional banking and it’s many failures.