Scrubbing Currency: A Comparison of Crypto to Fiat for Known Money Launderings.

Disclaimer: This article is for entertainment and general information purposes only. We do not make any guarantees that the information provided in this article is accurate or up to date. Always consult the appropriate professional legal console/attorneys, financial advisors, and tax specialists before making any business or financial decisions. We are not professional console, attorneys, financial advisors or tax specialists and the information provided in our articles does not constitute advice or guidance pertaining to the subjects we post about.. Do not make any decisions based on the information provided in this article as it may be inaccurate. You assume full risk if you decide to use any information from our website or this article for any purposes whatsoever. For full terms of service and policies please ensure you review them here: https://cryptobeadles.com/legal-policies/

Money laundering is a complex and intricate process intended to conceal illegally obtained money, often by transferring it through an involved sequence of commercial transactions or banking transfers—all with the intent to hide its true origin.

Criminal endeavors that generate a lot of cash usually promote the most egregious cases of money laundering. All that money has to be accounted for somehow, and law enforcement agencies are always on the lookout for large sums of money being transferred or deposited in banks with no clear source of origin. In order to access their ill-gotten gains without raising suspicion or calling attention to themselves, criminals have to invest considerable time and effort to obscure the true source of all that dirty money. Only after that money has been successfully “laundered” can it be safely used by the criminals or criminal organizations.

Law enforcement agencies around the world have instituted sophisticated anti-money laundering systems to spot and intercept transactions that raise suspicion.These agencies cooperate on an international basis to help each other detect “dirty” money circulating in the international banking sector.

Efforts to Curb Money Laundering

Anti-money laundering efforts examine any misuse of the financial system, including stocks and securities, cryptocurrency, traditional fiat currency, and even credit cards. In recent years, money laundering has been of increasing concern, as much of the proceeds of money laundering schemes have been tied to the funding of terrorist organizations world-wide.

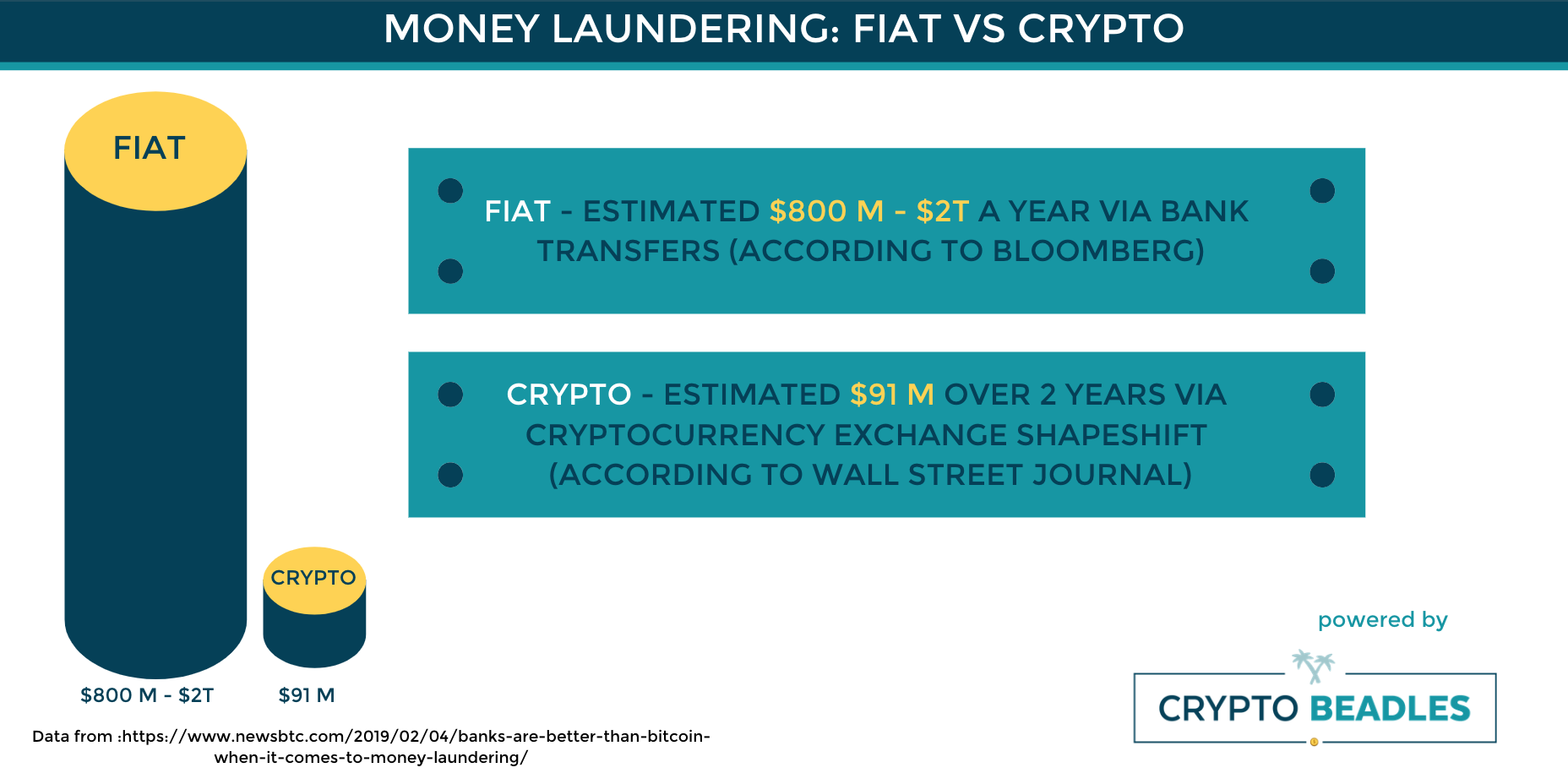

Money laundering however, seems almost commonplace. The Economist reported that the United Nations Office on Drugs and Crime estimates that between $800 billion and a staggering $2 trillion gets laundered each year. That’s a lot of money—between two to five percent of global gross domestic product. The growing internationalization of global currency trade makes money laundering even easier. Countries with bank-secrecy laws (like Switzerland, historically) can enable the transfer of large sums of money to countries that have bank-reporting laws, which enables criminals to deposit “dirty” money in one country and then transfer it to another—with no record of its origin required. In fact, some of the simplest money laundering schemes involve transferring money through several different countries to obscure its true origins.

Money laundering has been a problem for a long time, but it wasn’t always exactly illegal, at least not in the US. In 1986, the United States Congress passed an act called The Money Laundering Control Act, which criminalized money laundering in the US for the first time. It consists of two sections: one that prohibits individuals from giving or receiving money that was generated from a specific list of crimes, known in the Money Laundering Control Act as “specified unlawful activities,” or SUAs. The law also states that in order for financial transactions to fall under the heading of an SUA, the individual or individuals making the transaction must intend to conceal the source, ownership, or control of the funds—all things that money launderers seek to do. The second section of the law prohibits spending in any amount greater than $10,000 if the funds were derived from an SUA, regardless of whether an attempt is made to conceal the source or ownership of the funds.

Money Laundering and Fiat Currency

Up until recently, all the money laundering laws were focused on fiat currency. Fiat currency, if you’re not familiar with the term, might take a moment to understand. The word “fiat” comes from Latin and means “let it be done” or “it shall be.” Currency used to be “backed” by a physical commodity such as gold or silver. For instance, the English Pound—also called the Pound Sterling—is a promissory note that used to be worth exactly that: a pound of sterling silver.

Anyone who held a Pound Sterling note could go to a bank or exchange and trade that paper note for a pound of actual silver. The US dollar used to be backed by the “gold standard,” meaning any US currency could be traded, in theory, for a set amount of gold. The value of the dollar was intrinsically linked to the value of gold, and the exchange was seen to be “backed” by the commodity. The “silver standard” was another similar standard.

Up until 1971, the US government sold gold to foreign official holders of US dollars at the rate of $35 per ounce (which is astounding, when you think of today’s rates, which are in excess of a thousand dollars—a little over $1,300 as of this writing). After 1971, the US discontinued this practice, and in 1973 officially ended the gold standard. Thus, the US dollar was no longer reliant on a system of fixed exchange rates; the value instead became set by a system of floating rates. Most other countries followed suit, which is why the modern value of currency can (and does) fluctuate from day to day.

An interesting side note: prior to a presidential repeal in 1974, private citizens in the United States were prohibited from owning gold or engaging in transactions involving gold. Today, there are no countries that ban private ownership of gold—that went out when the “gold standard” died.

So, what we’re left with now is fiat currency. Not having any backing in physical commodities like gold or silver, the value of fiat currency is instead set by the laws of supply and demand—and the perceived stability of the issuing government. Almost all modern paper currencies are fiat currency.

In a nutshell, the value of fiat currency is determined by international agreements as to its worth. In other words, fiat, or “it shall be” currency is valued at exactly as much as various international bodies agree it’s worth. Nothing more.

The Rise of Cryptocurrency

Up until fairly recently, all anti-money laundering efforts have focused on fiat currency—because that’s all that existed. With the rise of cryptocurrency, new avenues and methods have become available to criminals interested in “scrubbing” the history or true origin of funds from financial transactions, thereby making use of the encrypted, decentralized nature of cryptocurrency markets. On the surface, cryptocurrency looks like the perfect solution to launder large sums of money with very little effort.

Here’s the thing though: cryptocurrency, due to the nature of the way it’s traded, might provide more effective methods of detecting and halting money laundering than any systems currently being used to combat the same thing with fiat currency.

Let’s focus for a moment on what cryptocurrency actually is. All cryptocurrencies are digital in nature—meaning they exist “virtually,” without any physical representation of the currency (other than some fleeting novelty production of physical tokens). As a purely digital type of currency, cryptocurrency relies on encryption techniques used to regulate the flow of transfers from one holder to another—and relies on the same type of encryption techniques for the generation of new units of cryptocurrency itself.

More to the point, the majority of cryptocurrency that exists is regulated and traded entirely independently of any central banking authority. Most cryptocurrencies are fully decentralized, and as such, one of the most democratized forms of currency that has ever been invented.

It is, in fact, very difficult to acquire cryptocurrency without first providing proof of your identity. All of the major cryptocurrency exchanges, partly in response to pressure being applied by various governmental bodies, have strict “know your customer” protocols in place that require would-be traders or holders of cryptocurrency to provide proof—usually in the form of government-issued identification cards—as to their real identity.

Cryptocurrency and World Governments: An Uneasy Truce

As cryptocurrency became more and more mainstream, thanks largely to the wild swings in the bitcoin market and speculation on its value as a long term investment, it captured the attention of world governments—perhaps precisely because it didn’t rely on centralized banking structures, and was therefore difficult (if not impossible) to regulate. Efforts to tax it have also proven to be difficult, but governments are figuring out ways to hold their citizens accountable.

There have been, especially in the past few years, numerous calls from financial institutions and governmental agencies for cryptocurrencies to institute regulations or systems to detect and prevent money laundering. This is especially a concern when it comes to the international drug trade.

Fiat vs Crypto: Built-In Tracking

As it turns out, it is much more difficult for criminals to hide the source and flow of cryptocurrencies than has been assumed. As stated above, it is next to impossible to acquire cryptocurrency without some form and binding proof of identity, and the very nature of cryptocurrency transactions, which relies on transfers to and from wallets identified by means of various digital markers, makes tracking cryptocurrency transactions all but automatic. Though there may exist ways to obfuscate or “tumble” crypto transactions, they are relatively easy to unravel by anyone who put the time and effort into doing so.

In fact, compared to traditional financial institutions, cryptocurrency has distinct advantages in keeping chains of transactions clear and visible. Each transaction is, by nature of the networks that handle them, public information. All anyone would need to “follow the money” would be the digital designation of the source of a transaction.

This is not the case with traditional banks. Transactions made using national or international banking organizations are protected by various privacy laws, and untangling a series of transfers and shifts would require search warrants or their international equivalent—and the cooperation of the banking entities involved.

The Traditional Banking Sector: A History of Failures

In fact, in December of 2018, the US Financial Industry Regulatory Authority (or FINRA) levied a $10 million fine on Morgan Stanley, the 38th largest bank in the world, for failure to comply with anti-money laundering legislation. This ordeal shatters the illusion that crypto exchanges are havens for criminals seeking to launder vast sums of illicitly acquired currency.

The cryptocurrency industry is run by smart people, people who recognize the value of validation and legitimacy. Every large exchange has progressively made its policies more in-line with defeating money laundering efforts before they can even take place, while the traditional banking world remains mired in outmoded, and difficult to change, regulations and practices.

That $10 million fine on Morgan Stanley was a result of an investigation that uncovered chronic and long-standing lapses in the giant bank’s anti-money laundering reporting system. As far back as 2011, Morgan Stanley suffered system failures of one kind or another which resulted in critically identifying customer information being lost or unrecorded. That resulted in a cascade of failures that made tens of billions of dollars of currency transfers and bank wires impossible to track. Any—or all—of that money could have been involved in money laundering schemes. It’s impossible to know.

The FINRA uncovered even more deficiencies in Morgan Stanley’s monitoring of stocks and commodity exchanges between 2011 and 2013, resulting in billions of shares of low-valued stocks being traded in a manner that had virtually no tracking or monitoring, which could have prevented the values of those stocks from being artificially (and illegally) inflated. Again, there is no way of telling what kind of malfeasance may have transpired.

It’s interesting to note that Morgan Stanley made no effort to deny or contest the charges and fines placed against it. Instead, they issued an understated but self-damning statement that read, “We are pleased to have resolved this matter from several years ago.”

And the problem isn’t just with American banks. In November of 2018, the Reserve Bank of India fined the German Deutsche Bank nearly half a million dollars for failing to properly identify customers involved in making deposits and transfers—and furthermore failing to accurately track the various subsequent movement of those traditional fiat currencies. At about the same time, the French banking institution Société Générale was charged $95 million for failure to comply with US anti-money laundering regulations—and was also faced with a larger $1.34 billion charge for breaking US trade sanctions against countries like Cuba, Iran, and Libya.

The following month, the Latvian bank BlueOrange faced a €1.2 million fine by that country’s financial regulating body for noncompliance with anti-money laundering regulations, and the US FINRA charged the Swiss bank UBS $5 million for its failure to adequately adhere to anti-money laundering systems.

In Conclusion

It is interesting to note that, to date, no cryptocurrency exchange has faced fines, reprimands, or legal action on any scale remotely similar to that faced by traditional banking institutions. This emphasizes the self-protective nature of cryptocurrency exchanges, the nature of the technology involved—which makes compliance with anti-money laundering regulations virtually effortless—and the fact that the traditional banking sector, mired in centuries of tradition and overly complicated systems of identifying customers, is a much more vulnerable venue for money laundering efforts.

If you’d like to learn more about blockchain technology, cryptocurrencies and how the industry is growing and changing, be sure to subscribe to Robert Beadles YouTube Channel Called CryptoBeadles. You can view his Channel here: https://www.youtube.com/cryptobeadles.

Robert also has an avid community he talks with regularly on his Telegram channel. You can join the conversion Too! Join the Crypto Beadles Telegram Channel here: https://t.me/Cryptobeadlesgroup